Insurance premiums soaring for Bay Area homeowners

TAMPA - Insurance premiums are soaring for Bay Area homeowners, and they could rise much more next year to cover losses from the hurricanes of 2024.

However, many customers don’t realize how much premiums can rise in a year, or how much less another provider may charge.

Dave Lesko and his father, Joe, moved from Georgia to a home in Dunedin, and initially could not believe the difference in process between the two states. Dave bought their house in 2021, and he’s a retired Colonel who applied his precision and discipline to renovating the home in 2022.

"I think everything we could have done to reinforce the home and update it from current standards is pretty much what we did," he said.

He spent around $100,000 bolstering the house to protect it from wind and water damage.

"We put all new hurricane windows (PG&T windows which are hurricane proof.) We reinforced the roof with straps," Lesko said. "And a system to take the water away from the house during a storm. We redid the plumbing in the whole house and added new sewage lines from the house to the street."

He also reduced the risk of fire.

"The electrician found some wires that weren't to code, so he recommended we rewire the whole house. It was easier to do it then, so we ended up rewiring the whole house."

After all that work and money, he looked forward to getting a break on his home insurance bill and ordered an inspection to bring it home.

In 2022, the year they renovated their home, insurance cost around $5,500. However, in 2023, instead of their rate dropping, they got dropped as customers.

And the cheapest replacement they could find cost around $7,500. That’s $2,000 more than what they were paying before the renovations.

At this point, he knew rates were soaring for most, and he hoped all the upgrades would at least keep their premium in check for 2024.

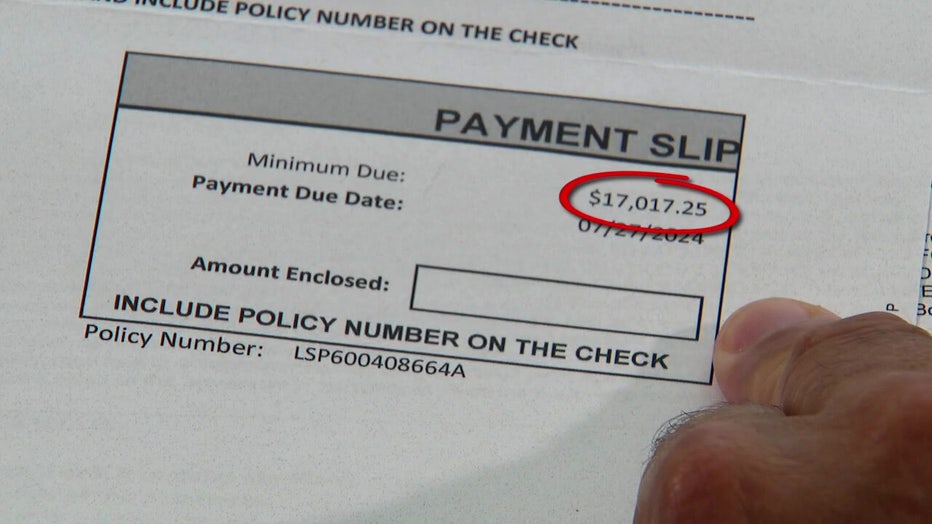

But when Dave finally got the renewal notice in the mail, his heart sank.

"Seventeen-thousand dollars" he said. "I had to get my glasses and double-check, but it's correct, and it’s actually a 120 percent increase from last year."

That’s around $10,000 dollars more than last year, and $12,000 more than what they paid just two years ago before a $100,000 in upgrades.

If you're wondering 'why' the price soared $10,000, we may never get a firm answer about that. The independent agent who lined up the policy could not say for sure.

"She said there were no notes on my file in terms of why they raised the price, but her belief was this company doesn't want to insure homes in Pinellas County," Lesko said.

We worked with Dave on shopping for other options. We found some in the private market starting around $8,700, but Dave decided to go with state-run Citizens Insurance for around $6,600.

That's two thousand less than the cheapest private coverage we could find, and a $1,000 less than what he had been paying.

For all the knocks on Citizens, the Insurance Information Institute said it can be the best deal in terms of money.

"It’s never necessarily about the price, although being budget conscious, you’re going to pick the price," said Mark Friedlander, Director of Corporate Communications for Insurance Information Institute. "For citizens, it’s very solid. You have very secure coverage with Citizens. Your claim will always be paid."

There are some catches. First, you're not allowed to get Citizens Insurance if a private company comes within 20% of the Citizens quote (which wasn't an issue for Dave). Second, a private company could pluck you out of the Citizens pool if they offer a quote up to 20% higher than what you’re paying. Third, with Citizens citizens, you run the risk of paying a surcharge up to 15% if major disasters strike and Citizens needs more money to pay all the claims. But even with a 15% surcharge, Dave still comes out a $1,000 ahead.

"My premium is less with Citizens and my coverage is higher so it’s better overall," said Lesko.

To keep Citizens next year, he'll also have to buy a separate flood policy next year under new state rules. That could cost around $900 more, but based on current rates, he'd still come out ahead and have flood coverage.

"Even with the new flood insurance requirement, typically you are going to be ahead in terms of total cost of insurance because Citizens rates run on average about 30-percent less in the private market," Friedlander noted.

The governor and legislative majority don't want people in the Citizens pool because it exposes the state to risk. And one too many disasters could eventually require a bailout from all policyholders. In the meantime, the same state leaders who don't want Citizens are also making it the best deal in town.

"The problem with Citizens is they're rate-restricted due to state regulations. They’re not allowed to charge actuarially sound rates, so they’ve been underselling the price of coverage," Friedlander explained.

For Joe and Dave and many others, that's a problem that currently works to their advantage—and it’s a big reason why Citizens (the so-called insurer of last resort) continues to add thousands of new customers a week.

Dave Lesko said he learned some important lessons as he worked through the process; know your policy renewal date and contact your insurance company 60 days before to check on the new rate, and shop rates. Get referrals from people you know.

Remember, independent agents write policies for a lot of companies, which helps you compare rates, but different independent agents also have different mixes of companies they work with. When you find your best option, be prepared to get a four-point inspection- because it may be required to get a new insurance policy.

STAY CONNECTED WITH FOX 13 TAMPA:

- Download the FOX Local app for your smart TV

- Download the FOX 13 News app for breaking news alert, latest headlines

- Download the SkyTower Radar app

- Sign up for FOX 13’s daily newsletter